Rising Interest Rates and the Impact on Real Estate Values. Is there a direct connection? In a post entitled Interest Rates and Property Values. What’s the Connection?, I suggested that there was. An example was given which suggested that mortgage lenders would be directly impacted by a rise in rates, as their underwriting parameters, most notably debt service coverage requirements, are directly impacted. An inability for a buyer to secure the required financing amount, in an environment of increasing interest rates will, I argue, impact their willingness to offer as high a purchase price. Arguably a lower debt level will necessitate a greater amount of equity. This directly diminishes an investors cash-on-cash return. The inevitable result will be a softening of values, since buyers will want to offer less.

Are there Other Factors?

The above noted rationale, for establishing the link between interest rates and values, does however ignore other factors which may impact market sentiment.

A recent study by Manulife Asset Management raises some interesting observations. In their March 2018 report entitled Canadian Commercial Real Estate Outlook, Manulife’s study observed that in fact there was no consistent relationship between real estate values and interest rates. One of their important findings was that although interest rates have been rising since November 2016, largely as a result of economic growth and higher inflationary pressure, capitalization rates actually declined. Why? Well apart from the sentiments of an individual buyer and lender, which is what I referenced in my earlier post, Canadian investors enjoyed improving real estate fundamentals. Yields were seen to be attractive in comparison to other investments, and there was a rise in foreign investment. All contributed to a support for commercial real estate fundamentals and stable or enhanced values.

Capitalization Rate Refresher

You may recall that capitalization rates are comprised of a nominal “risk-free” rate (often associated with a Government of Canada benchmark bond yield), plus a risk premium attributed to a specific property type or asset. If, as it appears, overall capitalization rates have declined, could it be that the “risk-free” rate is falling as well? I will encourage you to take a look at the Manulife report and come to your own conclusions. From a lender’s perspective, I do not doubt that rising rates have a bearing on what a buyer will pay for a property. I suspect real estate appraisers will be like-minded. The Manulife study does however caution us that there are macro-factors at play as well, and a strong economy is supportive of longer term stability, and indeed growth, in the Canadian Commercial real estate market.

National home sales rose by 4.1% in June compared to May, the first such rise this year. Even so, June’s sales activity remains well below the monthly pace of the past five years (see chart). The sales gains were led by the Greater Toronto Area (GTA) as 60% of all local housing markets reported increased existing home sales.

According to the Toronto Real Estate Board, sales were up 17.6% in the GTA on a seasonally adjusted basis between May and June.

In contrast, sales in British Columbia continued to moderate. The Real Estate Board of Greater Vancouver reported a 14.4% decline in home sales last month compared to the month before. June’s sales for the GVA were 28.7% below the 10-year June sales average. On a year-over-year (y/y) basis, sales declined a whopping 37.7%.

National home sales activity declined almost 11% y/y. Annual sales hit a five-year low and stood nearly 7% below the 10-year average for June. Activity came in below year-ago levels in about two-thirds of all local markets, led overwhelmingly by those in the Lower Mainland of British Columbia.

“This year’s new stress-test on mortgage applicants has been weighing on homes sales activity; however, the increase in June suggests its impact may be starting to lift,” said CREA President Barb Sukkau. “The extent to which the stress-test continues to sideline home buyers varies by housing market and price range.”

B.C. was hit with a double whammy as the province raised the foreign purchase tax as well. Also, mortgage rates have risen increasing the burden of the new stress tests.

Looking ahead, home sales and price gains will likely be dampened by higher interest rates as the Bank of Canada just hiked the benchmark rate once more last week. The prime rate rose from 3.45% to 3.70% in the wake of the rate hike, while the posted 5-year fixed mortgage rate–the critical stress-test yield–remained steady at 5.34%. Nevertheless, more upward pressure on mortgage rates is likely over the next couple of years as economic activity bumps up against capacity limits and inflation edges upward. The Bank made it very clear that further interest rate hikes are on the way but reiterated that it will be taking a gradual approach to future increases, guided by incoming economic data and a recognition that the economy is more sensitive to interest rate movements now than it was in the past.

New Listings

The number of newly listed homes fell in June by 1.8% and also remained below levels for the month in recent years. New listings declined in a number of large urban markets including those in B.C.’s Lower Mainland, Calgary Edmonton, Ottawa and Montreal.

With new listings up and sales virtually unchanged, the national sales-to-new listings ratio eased to 50.6% in May compared to 53.2% in April and stayed within short reach of the long-term average of 53.4%. Based on a comparison of the sales-to-new listings ratio with its long-term average, about two-thirds of all local markets were in balanced market territory in May 2018.

There were 5.7 months of inventory on a national basis at the end of May 2018. While this marks a three-year high for the measure, it remains near the long-term average of 5.2 months.

Home Prices

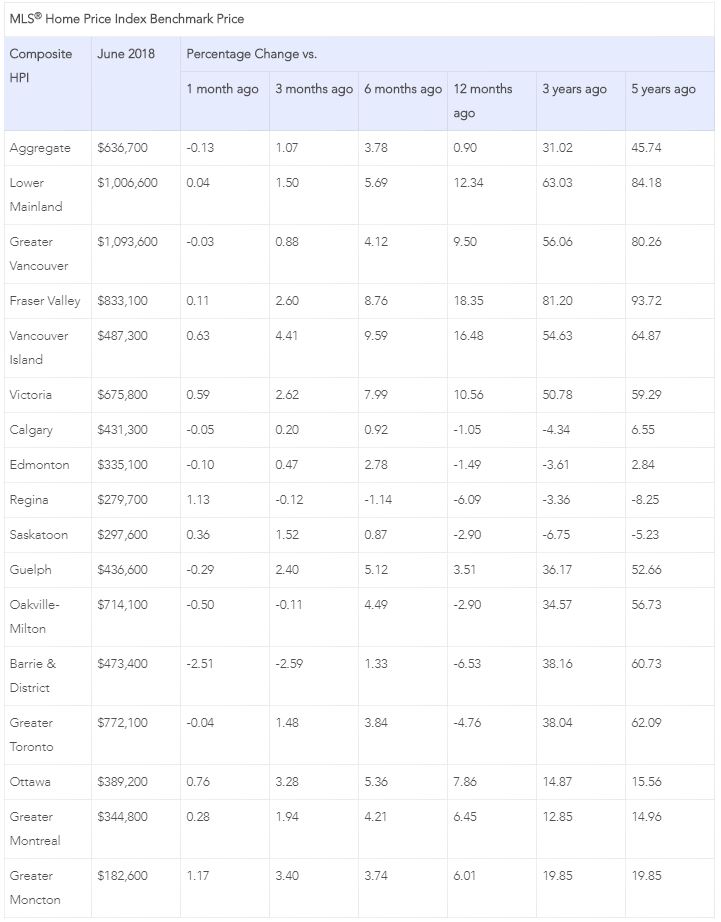

On a national basis, the Aggregate Composite MLS Home Price Index (HPI) rose only 0.9% y/y in June 2018, marking the 14th consecutive month of decelerating y/y gains. It was also the smallest annual increase since September 2009.

Decelerating y/y home price gains have reflected mainly trends at play in Greater Golden Horseshoe (GGH) housing markets tracked by the index. Home prices in the region have begun to stabilize and trend higher on a month-over-month basis in recent months.

Condo apartment units again posted the most substantial y/y price gains in June (+11.3%), followed by townhouse/row units (+4.9%); However, price gains for these homes have decelerated this year. By contrast, one-storey and two-storey single-family home prices were again down in June (-1.8% and -4.1% y/y respectively).

Benchmark home prices in June were up from year-ago levels in 8 of the 15 markets tracked by the index (see Table below).

Home price growth is moderating in the Lower Mainland of British Columbia (Greater Vancouver Area: +9.5% y/y; Fraser Valley: (+18.4%), Victoria (+10.6%) and elsewhere on Vancouver Island (+16.5%).

Within the GGH region, price gains have slowed considerably on a y/y basis but remain above year-ago levels in Guelph (+3.5%). By contrast, home prices in the GTA, Oakville-Milton and Barrie were down from where they stood one year earlier (GTA: -4.8%; Oakville-Milton: -2.9%; Barrie and District: -6.5%). The declines reflect rapid price growth recorded one year ago and masks recent month-over-month price gains in these markets.

Calgary and Edmonton benchmark home prices were down slightly on a y/y basis (Calgary: -1.0%; Edmonton: -1.5%), while prices declines in Regina and Saskatoon were comparatively more substantial (-6.1% and -2.9%, respectively).

Benchmark home prices rose by 7.9% y/y in Ottawa (led by a 9.1% increase in two-storey single-family home prices), by 6.4% in Greater Montreal (driven by a 7.4% increase in townhouse/row unit prices) and by 6% in Greater Moncton (led by a 6.5% increase in one-storey single-family home prices).

The actual (not seasonally adjusted) national average price for homes sold in June 2018 was just under $496,000, down 1.3% from one year earlier. While this marked the fifth month in a row in which the national average price was down on a y/y basis, it was the smallest decline among them.

The national average price is heavily skewed by sales in the Greater Vancouver and GTA, two of Canada’s most active and expensive markets. Excluding these two markets from calculations cuts almost $107,000 from the national average price, trimming it to just over $389,000.

Bottom Line

Housing markets continue to adjust to regulatory and government tightening as well as to higher mortgage rates. The speculative frenzy has cooled, and multiple bidding situations are no longer commonplace in Toronto and surrounding areas. The housing markets in the GGH appear to have bottomed, and supply constraints may well stem the decline in home prices in coming months. The slowdown in housing markets in the Lower Mainland of B.C. accelerated last month as the sector continues to reverberate from provincial actions to dampen activity, as well as the broader regulatory changes and higher interest rates.

Five-year fixed mortgage rates have already risen roughly 110 basis points, while rates for new variable mortgages rose by close to 40 basis points. Since the implementation of new mortgage standards, nonprice lending conditions for mortgages and home equity lines of credit have also tightened. Additional rate hikes by the Bank of Canada are coming, although the Bank will remain cautious particularly in light of continued trade tensions with the United States.

Dr.Sherry Cooper

Chief Economist, Dominion Lending Centres

Sherry is an award-winning authority on finance and economics with over 30 years of bringing economic insights and clarity to Canadians.

Since becoming a broker, the words “interest rate” have been haunting me. It’s the one topic every client is sensitive about.

With the exception of a few of my clients who had little choice, majority have elected to take advantage of the great variable rates, sometimes after significant convincing.

Most people believe The Bank of Canada is expected to boost a key interest rate tomorrow as it continues its efforts to “wean” the economy off low borrowing costs.

The bank’s target for the overnight rate — what major financial institutions charge each other for one-day loans —has been at 1.25 per cent since mid-January. Since then, the bank has stood firm on three subsequent rate announcements. That is expected to end tomorrow at 10AM with an estimated probability of 96 per cent, according to Bloomberg.

So what does this mean for my clients? Well, for those in a variable rate product, you will NOT see any payment increase in your mortgage, however, the amount of your total payment that is applied against your principle, will be slightly reduced, extending the total amortization of your mortgage. Luckily, my clients have also usually been convinced to take advantage of their prepayment options and are already adding an extra hundred or so to each of their payments.

For those in an Adjustable Rate Mortgage, you will see a monthly increase of about 10 dollars for every $100,000 you owe on your mortgage. Considering, you’ve already been saving nearly $40.00 per 100K in mortgage, you’re still in the black, and will be for some time.

Conclusion – Don’t jump the gun, and don’t think with emotions. Rate doesn’t need to be the next 4-letter swear word for homeowners. If you are in a Variable or Adjustable rate mortgage, you are still ahead of those in a fixed rate mortgage. No matter what your grandparents might say.

Hold your course – and don’t lock in your rates! If you need help walking away from the edge or need some more convincing, give me a call.

Richard de Chevigny, PMP

Mortgage Expert

Dominion Lending Centres – Red River Lending

With all of the rule changes imposed by the federal and provincial governments around mortgage financing and real estate it may be more difficult to access financing. But don’t take it personally – sometimes it’s not you it’s the property.

When lenders underwrite your application for approval they look at you as a borrower but they also evaluate the property.

Here are some things to consider before you purchase.

The type of property — house, condo, duplex, heritage, etc.

Especially for condo properties the lender (and insurer if required) will look at the age of the building, the history of maintenance or lack there of and the location for marketability. Some lenders will limit their exposure with a maximum number of units in a building or avoid lending on buildings after a certain age for the property.

Properties with more than 4 units in them such as a 5-plex will be considered commercial real estate and the lender will evaluate on that basis.

Heritage homes (registered or designated) require a more detailed review and special consideration for financing.

Leasehold and co-op properties also have specific requirements for the maximum loan to value so more down payment may be required. More documentation will be required and interest rates will vary.

The location of the property— lenders always consider their risk in each market.

If the location limits the potential resale value for the building in the event of default by the borrower they may not lend on that property. Some lenders will reduce the loan amount for a building located out of major market areas or add a premium to the interest rate.

For properties with water access only or with no access to municipal utilities (water, heat, light and sewer) more details are required to assess the lender risk. Insurance coverage, water testing, seasonal access and condition of the property will be strong considerations.

The use for the property— personal or investment, recreational, previous activities.

If the owner occupied house has a suite then rental income may be considered.

If the house is purchased for investment then rental income is considered and the interest rate for rental rather than owner occupied is assigned. In these cases the rental income can increase the resale value of the property. However, the appraisal of the property will be reviewed to ensure the condition of the property and if any renovations were completed to add value.

There are lending options for a previous grow-op that come with higher interest rates and costs

In the case of a condo the property may have a commercial component in the building (shops below) or allowable space in the unit for business (live/work designation). In these cases some lenders may not have an appetite for financing. In some cases the lender may allow with approval by the insurer (CMHC, etc).

Purchasing a second home for recreational use will require a review if it is seasonal or year-round access.

If the property requires renovations the extent and cost to value of the property will be considered.

It is very important before you start looking at any property to talk with a Dominion Lending Centres mortgage broker. This allows you to discuss the specific requirements for any variation in the type of property you may want to purchase and allow ample time for a full financing review before subject removal on a purchase.

For example:

If you shift from a standard condo to a lease-hold property your down payment amount will likely change.

If you want to move to a small rural town or to a small island you may have to pay a higher rate or have less options and more documentation required on the property.

If you buy a home in one province but may be transferred to another province, some lenders such as credit unions are provincially based so you can’t port the mortgage.

If the condo you wish to buy has no deprecation report, a low contingency fund or big special levies pending, these will all be a red flag for the lender and should be a strong consideration for you as a buyer. A more thorough review will be required.

Always consult an experienced independent mortgage broker as your trusted advisor for all of your financing needs. You will appreciate the difference in the level of expertise to help you make an informed decision.

Insurance coverage is something that everyone is “pitched” at some point or another in their life. Unfortunately, a lot of us have a negative attitude towards insurance or warranty as it is perceived as being a cash grab. Yes, if you are purchasing a flat screen T.V., that extra 2-year warranty for $100 might be a little excessive. However, when it comes to covering monthly mortgage payments or the outstanding balance of your mortgage upon death or injury, yes, it is important to have.

Every single person is offered life and disability insurance when applying for a new mortgage. As a mortgage broker, it is our obligation to offer you Manulife’s Mortgage Protection Plan. Even if it is something you do not want or do not have a need for- we still require a signature confirming it was offered. Reason being, is when John Smith breaks his foot two years down the road and can’t work to cover his mortgage payments, Manulife needs to confirm that the client passed on the opportunity to have their payments covered.

Now, is Manulife’s mortgage Protection Plan, or, MPP as it is known, the most comprehensive coverage out there? No.

Is MPP better than any coverage you are ever going to receive from a bank directly? Yes.

Manulife’s MPP is a 60-day money back guarantee, with coverage that follows you lender to lender. It will cover disability injuries preventing you from work, and is underwritten before your coverage begins, not when a claim is made.

Most banks do not allow you to take their mortgage insurance to another lender. So, if after 10-years of paying your premiums you decide to leave your bank and go to a credit union, your coverage is no longer in affect and all that money you spent on your monthly premiums is now worth nothing. Scariest part about bank coverage, is the health evaluation is done when a claim is made, not when you sign up. Can you imagine not making a claim for 20-years and then being declined on coverage because you have developed health issues not relevant when you signed up in your 20’s?

If Manulife Mortgage Protection Plan is not for you, there are insurance brokers out there we have access to who can offer alternative solutions. The biggest thing though is to make sure you have SOME coverage, because you won’t know you need it until you do. If you have any questions, contact a Dominion Lending Centres mortgage professional for help.