You may have already seen the more technical BANK OF CANADA RATE ANNOUNCEMENT on October 24th, or you may not have. The Coles Notes (the simplest version) are as such:

Global economy remains strong, the USMCA will reduce trading uncertainty

Canadian economy is balanced for the foreseeable 2 years

Household spending will increase, but backed by income growth

Housing activity across Canada is stabilizing

On October 24th the Bank of Canada did what we all expected, they increased the Overnight lending rate by 0.25% to 1.75%. This equated to a PRIME being increased by 0.25% to 3.95%. All variable rate mortgages and lines of credit utilize PRIME to calculate the current interest rate.

Now the BIG QUESTION, how do we as mortgage consumers respond? First, ask your Dominion Lending Centres mortgage broker how they plan to react in accordance to his own financing.

No need to ask me, I will tell you. Variable, with no hesitation. I will stay the course by not pushing the panic button.

WHY?

Because if I decide to move, re-finance, consolidate, leverage equity or to simply break the mortgage for any reason my penalty will only be 3 months interest. I also need to consider how much money I have saved over the term by utilizing a variable rate mortgage rather than a fixed. During my current mortgage the spread between variable and fixed is approximately 1%.

Please excuse the following ‘tongue & cheek…’To go with a fixed mortgage tells me that you can predict the future with absolute certainty.

I know I can’t, so I rely on statistics. 65% of all fixed mortgage consumers will break their mortgage in 33 months, the penalty that follows is unavoidable. For the average B.C. mortgage of $350,000 the penalty is approximately $14,000. By opting for a fixed rate mortgage, you have declared to the universe that there is a zero percent chance you will need to access equity, amend the current mortgage or consider applying for a secured line of credit.

Real estate wealth is a long game, building net worth doesn’t happen overnight. Gains are not made in the short term. Just like other markets (stocks, bonds, mutuals, GICs RRSPs), there will be highs and lows.

What does this increase mean?

Dollarize it for your own personal consumption. For an increase of 0.25% the payment will go up $13 per every $100,000 borrowed. For some variable rate borrowers, the payment hasn’t even changed as the lender only adjusts the principal and interest allocation.

Now the question becomes, what do you do? Remain with variable or lock into a fixed. I recommend staying the course.

esterday, The Bank of Canada maintained its target for the overnight rate at 1 ½ per cent. The Bank Rate is correspondingly 1 ¾ per cent and the deposit rate is 1 ¼ per cent.

CPI inflation moved up to 3 per cent in July. This was higher than expected, in large part because of a jump in the airfare component of the consumer price index. The Bank expects CPI inflation to move back towards 2 per cent in early 2019, as the effects of past increases in gasoline prices dissipate. The Bank’s core measures of inflation remain firmly around 2 per cent, consistent with an economy that has been operating near capacity for some time. Wage growth remains moderate.

Recent data on the global economy have been consistent with the Bank’s July Monetary Policy Report (MPR) projections. The US economy is particularly robust, with strong consumer spending and business investment. Elevated trade tensions remain a key risk to the global outlook and are pulling some commodity prices lower. Meanwhile, financial stresses have intensified in certain emerging market economies, but with limited spillovers to other countries.

The Canadian economy is evolving closely in line with the Bank’s July projection for growth to average near potential. Following growth of 1.4 per cent in the first quarter, GDP rebounded by 2.9 per cent in the second quarter, as the Bank had forecast. GDP growth is expected to slow temporarily in the third quarter, mainly because of further fluctuations in energy production and exports.

While uncertainty about trade policies continues to weigh on businesses, the rotation of demand towards business investment and exports is proceeding. Despite choppiness in the data, both business investment and exports have been growing solidly for several quarters. Meanwhile, activity in the housing market is beginning to stabilize as households adjust to higher interest rates and changes in housing policies. Continuing gains in employment and labour income are helping to support consumption. As past interest rate increases work their way through the economy, credit growth has moderated and the household debt-to-income ratio is beginning to edge down.

Recent data reinforce Governing Council’s assessment that higher interest rates will be warranted to achieve the inflation target. We will continue to take a gradual approach, guided by incoming data. In particular, the Bank continues to gauge the economy’s reaction to higher interest rates. The Bank is also monitoring closely the course of NAFTA negotiations and other trade policy developments, and their impact on the inflation outlook.

Here are the remaining announcements dates for 2018.

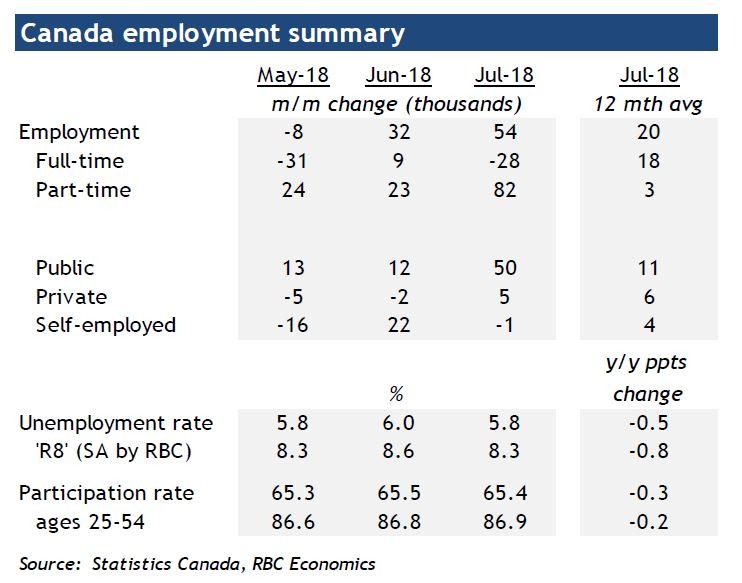

Statistics Canada announced this morning that employment increased in July and the jobless rate fell .2 percentage points to 5.8%–returning to its lowest level since the 1970s posted earlier this year.

The economy added a stronger-than-expected 54,100 net new jobs last month–its most significant advance this year. This gain, however, was driven by increases in part-time work. July’s jobs surge followed the 31,800 rise in June. Both months enjoyed advances well above the 20,000 average monthly gains of the past year.

In the 12 months to July, employment grew by 246,000 (+1.3%), largely reflecting growth in full-time work (+211,000 or +1.4%). Over this period, the total number of hours worked rose by 1.3%.

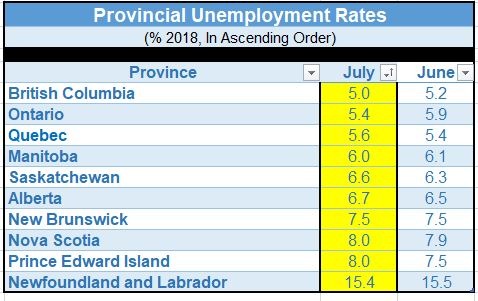

The job growth last month was primarily in public sector jobs, especially in educational services mainly in Ontario and Quebec. At the national level, the rise was primarily in employment in post-secondary institutions, particularly universities, and was mostly in part-time work. The number of people working in health care and social assistance also rose, mainly in Ontario. In British Columbia, the number of people working increased by 11,000 and the jobless rate was 5.0% (see table below). Job gains were also noted in Newfoundland and Labrador, the first increase since October 2017. The number of workers declined in Saskatchewan and Manitoba, while it was little changed in other provinces.

Manufacturing jobs declined by 18,400 in contrast to the record-high jump of 90,500 in the service sector. The surge in service sector employment, however, likely reflected a technical distortion. The timing of hiring in the education sector has been volatile over the summer months in recent years causing a seasonal adjustment problem. The July spike education jobs will likely be unwound in the next two months.

Wags gains slowed during the month, with average hourly wages up 3.2% y/y compared to 3.6% y/y in June. Wage gains for permanent workers were 3%, the slowest this year.

The Canadian economy continues to run at a stronger pace than long-run potential as the labour markets continue to tighten. The jobless rate of 5.8% is below the full-employment level of 6.0%-to-6.5%. A more robust pace of hiring runs the risk of further increasing excess demand, putting upward pressure on inflation. In consequence, the Bank of Canada will continue to withdraw stimulus by gradually hiking overnight rates.

This report has raised the likelihood of another increase in the benchmark overnight rate of 25 basis points, possibly as soon as the next policy meeting in September. Inflation, however, remains at the Bank of Canada’s target of 2.0%, allowing the Bank to wait until the subsequent meeting in October.

DR. SHERRY COOPER

Chief Economist, Dominion Lending Centres

Sherry is an award-winning authority on finance and economics with over 30 years of bringing economic insights and clarity to Canadians.

National home sales rose by 4.1% in June compared to May, the first such rise this year. Even so, June’s sales activity remains well below the monthly pace of the past five years (see chart). The sales gains were led by the Greater Toronto Area (GTA) as 60% of all local housing markets reported increased existing home sales.

According to the Toronto Real Estate Board, sales were up 17.6% in the GTA on a seasonally adjusted basis between May and June.

In contrast, sales in British Columbia continued to moderate. The Real Estate Board of Greater Vancouver reported a 14.4% decline in home sales last month compared to the month before. June’s sales for the GVA were 28.7% below the 10-year June sales average. On a year-over-year (y/y) basis, sales declined a whopping 37.7%.

National home sales activity declined almost 11% y/y. Annual sales hit a five-year low and stood nearly 7% below the 10-year average for June. Activity came in below year-ago levels in about two-thirds of all local markets, led overwhelmingly by those in the Lower Mainland of British Columbia.

“This year’s new stress-test on mortgage applicants has been weighing on homes sales activity; however, the increase in June suggests its impact may be starting to lift,” said CREA President Barb Sukkau. “The extent to which the stress-test continues to sideline home buyers varies by housing market and price range.”

B.C. was hit with a double whammy as the province raised the foreign purchase tax as well. Also, mortgage rates have risen increasing the burden of the new stress tests.

Looking ahead, home sales and price gains will likely be dampened by higher interest rates as the Bank of Canada just hiked the benchmark rate once more last week. The prime rate rose from 3.45% to 3.70% in the wake of the rate hike, while the posted 5-year fixed mortgage rate–the critical stress-test yield–remained steady at 5.34%. Nevertheless, more upward pressure on mortgage rates is likely over the next couple of years as economic activity bumps up against capacity limits and inflation edges upward. The Bank made it very clear that further interest rate hikes are on the way but reiterated that it will be taking a gradual approach to future increases, guided by incoming economic data and a recognition that the economy is more sensitive to interest rate movements now than it was in the past.

New Listings

The number of newly listed homes fell in June by 1.8% and also remained below levels for the month in recent years. New listings declined in a number of large urban markets including those in B.C.’s Lower Mainland, Calgary Edmonton, Ottawa and Montreal.

With new listings up and sales virtually unchanged, the national sales-to-new listings ratio eased to 50.6% in May compared to 53.2% in April and stayed within short reach of the long-term average of 53.4%. Based on a comparison of the sales-to-new listings ratio with its long-term average, about two-thirds of all local markets were in balanced market territory in May 2018.

There were 5.7 months of inventory on a national basis at the end of May 2018. While this marks a three-year high for the measure, it remains near the long-term average of 5.2 months.

Home Prices

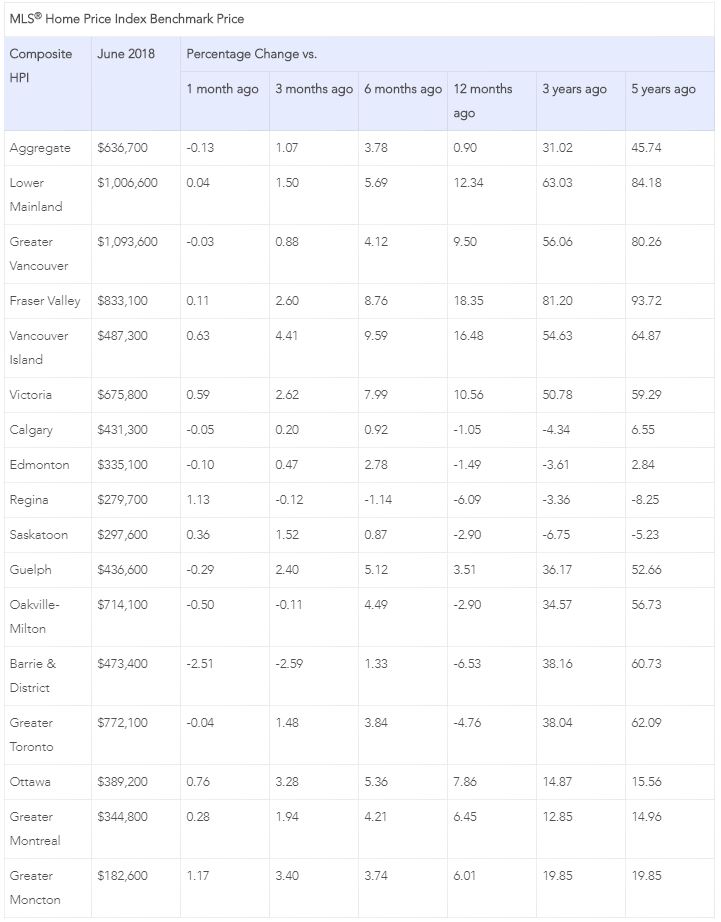

On a national basis, the Aggregate Composite MLS Home Price Index (HPI) rose only 0.9% y/y in June 2018, marking the 14th consecutive month of decelerating y/y gains. It was also the smallest annual increase since September 2009.

Decelerating y/y home price gains have reflected mainly trends at play in Greater Golden Horseshoe (GGH) housing markets tracked by the index. Home prices in the region have begun to stabilize and trend higher on a month-over-month basis in recent months.

Condo apartment units again posted the most substantial y/y price gains in June (+11.3%), followed by townhouse/row units (+4.9%); However, price gains for these homes have decelerated this year. By contrast, one-storey and two-storey single-family home prices were again down in June (-1.8% and -4.1% y/y respectively).

Benchmark home prices in June were up from year-ago levels in 8 of the 15 markets tracked by the index (see Table below).

Home price growth is moderating in the Lower Mainland of British Columbia (Greater Vancouver Area: +9.5% y/y; Fraser Valley: (+18.4%), Victoria (+10.6%) and elsewhere on Vancouver Island (+16.5%).

Within the GGH region, price gains have slowed considerably on a y/y basis but remain above year-ago levels in Guelph (+3.5%). By contrast, home prices in the GTA, Oakville-Milton and Barrie were down from where they stood one year earlier (GTA: -4.8%; Oakville-Milton: -2.9%; Barrie and District: -6.5%). The declines reflect rapid price growth recorded one year ago and masks recent month-over-month price gains in these markets.

Calgary and Edmonton benchmark home prices were down slightly on a y/y basis (Calgary: -1.0%; Edmonton: -1.5%), while prices declines in Regina and Saskatoon were comparatively more substantial (-6.1% and -2.9%, respectively).

Benchmark home prices rose by 7.9% y/y in Ottawa (led by a 9.1% increase in two-storey single-family home prices), by 6.4% in Greater Montreal (driven by a 7.4% increase in townhouse/row unit prices) and by 6% in Greater Moncton (led by a 6.5% increase in one-storey single-family home prices).

The actual (not seasonally adjusted) national average price for homes sold in June 2018 was just under $496,000, down 1.3% from one year earlier. While this marked the fifth month in a row in which the national average price was down on a y/y basis, it was the smallest decline among them.

The national average price is heavily skewed by sales in the Greater Vancouver and GTA, two of Canada’s most active and expensive markets. Excluding these two markets from calculations cuts almost $107,000 from the national average price, trimming it to just over $389,000.

Bottom Line

Housing markets continue to adjust to regulatory and government tightening as well as to higher mortgage rates. The speculative frenzy has cooled, and multiple bidding situations are no longer commonplace in Toronto and surrounding areas. The housing markets in the GGH appear to have bottomed, and supply constraints may well stem the decline in home prices in coming months. The slowdown in housing markets in the Lower Mainland of B.C. accelerated last month as the sector continues to reverberate from provincial actions to dampen activity, as well as the broader regulatory changes and higher interest rates.

Five-year fixed mortgage rates have already risen roughly 110 basis points, while rates for new variable mortgages rose by close to 40 basis points. Since the implementation of new mortgage standards, nonprice lending conditions for mortgages and home equity lines of credit have also tightened. Additional rate hikes by the Bank of Canada are coming, although the Bank will remain cautious particularly in light of continued trade tensions with the United States.

Dr.Sherry Cooper

Chief Economist, Dominion Lending Centres

Sherry is an award-winning authority on finance and economics with over 30 years of bringing economic insights and clarity to Canadians.

Since becoming a broker, the words “interest rate” have been haunting me. It’s the one topic every client is sensitive about.

With the exception of a few of my clients who had little choice, majority have elected to take advantage of the great variable rates, sometimes after significant convincing.

Most people believe The Bank of Canada is expected to boost a key interest rate tomorrow as it continues its efforts to “wean” the economy off low borrowing costs.

The bank’s target for the overnight rate — what major financial institutions charge each other for one-day loans —has been at 1.25 per cent since mid-January. Since then, the bank has stood firm on three subsequent rate announcements. That is expected to end tomorrow at 10AM with an estimated probability of 96 per cent, according to Bloomberg.

So what does this mean for my clients? Well, for those in a variable rate product, you will NOT see any payment increase in your mortgage, however, the amount of your total payment that is applied against your principle, will be slightly reduced, extending the total amortization of your mortgage. Luckily, my clients have also usually been convinced to take advantage of their prepayment options and are already adding an extra hundred or so to each of their payments.

For those in an Adjustable Rate Mortgage, you will see a monthly increase of about 10 dollars for every $100,000 you owe on your mortgage. Considering, you’ve already been saving nearly $40.00 per 100K in mortgage, you’re still in the black, and will be for some time.

Conclusion – Don’t jump the gun, and don’t think with emotions. Rate doesn’t need to be the next 4-letter swear word for homeowners. If you are in a Variable or Adjustable rate mortgage, you are still ahead of those in a fixed rate mortgage. No matter what your grandparents might say.

Hold your course – and don’t lock in your rates! If you need help walking away from the edge or need some more convincing, give me a call.

Richard de Chevigny, PMP

Mortgage Expert

Dominion Lending Centres – Red River Lending

Some of the last round of changes from the government regarding qualifying for a mortgage were that if you have a balance on your unsecured line of credit, then to qualify for mortgage the lenders require that we use a 3% payment of the balance of the line of credit.

Simple math is, if you owe $10,000 we have to use $300 as your monthly payment regardless of what the bank requires as a minimum. Given that the banks hand out lines of credit on a regular basis it is not uncommon for us to see $50,000 lines of credit with balances in the $40,000 range. That amount then means we have to use $1,200 a month as a payment even though the bank may require considerably less.

So what if it is a secured line of credit? Again we have clients telling us that they don’t have a mortgage only to realize they do have a Home Equity Line of Credit (HELOC). A home equity line of credit by all definition is a loan secured by property, the actual definition of a mortgage.

Again, it’s something the bank will require little more than interest payment on because it is secured. The calculation here can also upset the calculation for your next mortgage, as what is required by many lenders is to take the balance of the HELOC. Let’s say the balance is $200,000 and you convert it to a mortgage at the bench mark rate, which today is 5.34% with a 25-year amortization. That without any fees today is equal to $1202.22 per month, so what in the client’s mind may be a $400 or $500 dollar interest payment for the purpose of qualifying will be almost three times higher.

This one change to supposedly safe guard the Canadian consumer has lately been the thing we have seen stop more mortgages than just about anything else. If you have any question, contact a Dominion Lending Centres mortgage professional for answers.

The Federal Open Market Committee (FOMC) met this week for the second time under the chairmanship of Jerome Powell. In a unanimous decision, the Committee left the target range for the federal funds rate unchanged at 1-1/2 to 1-3/4 percent. Unlike the Bank of Canada, which has a single objective of targeting inflation at roughly 2 percent, the Fed has a dual statutory mandate to both foster price stability and maximum employment.

U.S. labour conditions remain strong, and the economy continues to grow at a moderate pace. Inflation has now moved to close to 2 percent. The growth of household spending has moderated from their strong fourth-quarter pace, although business fixed investment continued to grow rapidly.

“The Committee expects that economic conditions will evolve in a manner that will warrant further gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.”

The yield on 10-year U.S. Treasury notes slipped slightly to 2.96 percent following the release of the statement, while the S&P 500 Index of U.S. stocks climbed to its highest level of the day and the Bloomberg Dollar Spot Index fell.

U.S. economic growth cooled in the first quarter to an annualized pace of 2.3 percent after averaging higher than 3 percent in the previous three quarters.

Expectations are that the Fed will hike rates once again at the next meeting in June. The Fed signaled in March that they expect to raise rates three or four times this year. They hiked the target federal funds rate three times last year and began to gradually reduce their holdings of securities.

The Bank of Canada will likely raise rates twice this year–probably in the summer and fall. As always, central bank policy will remain data dependent and will adjust with any significant changes in the economic backdrop. It is widely expected that the NAFTA negotiations will be satisfactorily completed in the near future, but that still remains a wildcard.

Increased U.S. protectionist fervour is a significant negative for the global economy. Today, 1,100 U.S. economists signed a letter to President Trump warning him of the dangers of tariffs, reminding him that the 1930 Smoot-Hawley tariffs led to a sustained economic depression.

Chief Economist, Dominion Lending Centres

Sherry is an award-winning authority on finance and economics with over 30 years of bringing economic insights and clarity to Canadians.

This article appears in the April issue of Our House Magazine

Looking back at predictions from 50 years ago of what a home would look like and be able to do today, it’s almost laughable. Back then, the home of the future would include rooftop pools that act as air conditioners and a garage for our airplane automobile that has folding wings. Fast forward 50 years from now and depending on where you live in the future, a garage for your car may not even be needed.

Dave Pedigo is the VP of Emerging Technologies with CEDIA, a North American association representing the home technology industry. In 50 years from now, he believes homes will be filled with artificial intelligence, doing things we could only dream of today. The home will know what you like and don’t, where you spend more time and adjust accordingly. Don’t like doing laundry? You might not be alive to see it, but your offspring probably won’t have to worry too much about the annoying chore. There will be one machine that washes, dries and folds all your laundry and a robot to put it away.

Pedigo also predicts the future home will know your health better than you, calculating when you’re on the path to a catastrophic event like a heart attack days before, all while calling emergency services when needed.

“It’s going to be an incredibly, incredibly intelligent home,” he told Our House Magazine. “It will make our lives a lot easier.” While some of that technology is a lifetime away, some of it is closer than you think.

Pedigo explained a couple years back, CEDIA had an opportunity to design and display a home of the future for an exhibition. The home included a concrete wall that will appear invisible. With a touch of a button, the wall will come alive giving you the opportunity to display anything, even the previous day’s weather if you wanted. That feature may only be 10 years away.

“I think in general the goal is to make the home more comfortable, more enjoyable and healthier,” Pedigo said. “By the time we get to 50 years from now, it’s going to be amazing.” Pedigo also noted new technology tends to start off being for the wealthy, but quickly expands to the masses at a much cheaper cost.

We know technology will be a big part of homes, but they still have to be constructed. And the bones of a home will also look very different in the future.

Larry Stadnick has been building custom homes in the Calgary area for decades under his company Corey Homes. He believes homes in the future will be sleek, smaller and very efficient. The builder also sees homes getting boxier, flatter and similar to the mid-century modern style.

The trend Stadnick noted is to build the shell of the home using the insulated concrete form (ISF) which makes the home more energy efficient, quieter and stronger in a natural disaster. The

ICF is basically a cinder block, surrounded by Styrofoam with concrete in the middle. About 30 per cent of new homes in Calgary use the ICF today with that number expected to grow to 40 per cent in the next five years, according to Stadnick.

“With ICF you can control everything, you have total control of the environment [in the home],” he said.

If you talk to anyone with a heritage home built about 100 years ago, they’ll swear the quality of the home is far superior to anything new. But Stadnick sees it very differently, arguing the traditional wood frame home “sucked”, adding their construction was dependent on the forest industry, and how they would react in the weather.

While the latest technology may improve the home in a number of ways, it’s not particularly cheap. And cost is partly why Stadnick also suggests homes in the future, especially single-family homes, will be much more expensive.

“I’d be buying one now if I was a young kid,” he said, adding the cost of material and available land will also continue to rise. The insides of homes in the future will also be healthier.

The Calgary home builder noted the construction industry is already staying away from certain plastics and materials that can be toxic.

Meanwhile, the organization tasked with representing the residential construction industry in Canada is also looking toward the future.

David Foster, a spokesperson for the Canadian Home Builders’ Association, said his organization is working on new national building codes that will come into place in the 2030s.

He too sees a home that will be extremely energy efficient and safer to live.

The CHBA already has a program in place called Net Zero Housing, where the home generates as much energy as it consumes.

As for safety, Foster pointed out the number of residential fires has plummeted in recent decades and the trend will continue.

“We’re building homes that are more comfortable, healthier to live in, and that will just continue,” Foster said.

The single-family home could also be an endangered species 50 years from, especially in urban areas. With millions of people expected to flood the larger population centres, the CHBA, believes the majority of homes will be multi-unit developments near transit.

But back in Calgary, Stadnick jokes he won’t be around in 50 years to see the home of the future, although he’s confident they’ll be better than today and people will enjoy them just as much. “I’ve lived in more than 30 new homes and every one of them was exciting, and new and fresh and fun.”

The Canadian dollar fell sharply immediately after the release of the Bank of Canada’s Official Statement providing a more bullish forecast for the economy while holding rates steady. The Bank hiked its estimate of noninflationary potential growth, implying there was more room to grow without triggering rate hikes. The central bank now suggests the economy has a noninflationary speed limit of 1.8% this year and next, accelerating to 1.9% in 2020. Formerly, the Bank had estimated potential growth to average about 1.6% for the next two years.

Many market participants had expected a more hawkish statement as inflation has risen to close to the Bank’s 2%-target in recent months. The central bank appears to be straddling the fence, suggesting that rate hikes are coming, but the economy still needs stimulus. The good news is that growing demand is generating new capacity as businesses invest to meet sales, a development that Governor Poloz says the central bank has an “obligation” to nurture.

The Monetary Policy Report (MPR) notes that three-quarters of industries have a capacity utilization rate within five percentage points of their post-2003 peak. The business outlook survey, meanwhile, indicates that sales expectations have firmed. Taken together, this implies that there’s a real need for investment to meet higher demand.

The chief concern is that protectionism, which remains the central bank’s top risk to the outlook, coupled with the U.S. tax overhaul means businesses will choose to expand capacity outside of Canada. A “wide range of outcomes” is still possible for the NAFTA, according to the MPR, which did not acknowledge recently reported progress in talks between Canada, Mexico, and the U.S.

The central bank now sees first-quarter growth at 1.3%, down from a January forecast of 2.5%. Forecasts for 2018 were also brought down to 2%, from 2.2%. But 2019 growth was revised up to 2.1% from 1.6%. This stronger growth profile reflects upward revisions to the U.S. fiscally induced expansion.

Slower growth in the first quarter primarily reflected weakness in two areas. Housing markets slowed in the wake of the new mortgage guidelines. Exports also slowed, in part owing to transportation bottlenecks.

Concerning housing, the Monetary Policy Report contained an interesting chart (below) showing the cumulative change in housing resales since January 2017 with the following comment: “Housing activity is estimated to have contracted sharply in the first quarter, following the implementation of the revised B-20 Guideline. The contraction was amplified as some homebuyers acted quickly in the fourth quarter of 2017 to purchase a home before being subject to the new measure. In the second quarter of 2018, housing activity is expected to pick up as resales start to recover.”

Bottom Line: Despite upward revisions to inflation, the Bank’s assessment seems to be relatively sanguine. I expect two more quarter-point rate hikes this year–likely in the summer and fall.

Chief Economist, Dominion Lending Centres

Sherry is an award-winning authority on finance and economics with over 30 years of bringing economic insights and clarity to Canadians.

The mortgage industry is a fluid and ever-changing industry. What was applicable one day seems to no longer apply to the next, and at times, it can be confusing to navigate through what all of these changes mean–and how they impact you directly. As Mortgage Brokers, we firmly believe that although the industry has gone through many changes over the years, each time our clients are able to overcome them by practicing the same sound advice–which we will reveal at the end! But first, a walkthrough of the mortgage changes over the past few years and how the industry has changed:

LOOKING BACK

Before 2008

During this time, lending and mortgages policies were much more lenient! There was 100% financing available, 40-year amortizations, cash back mortgages, 95% refinancing, 5% down payment required for rental properties, and qualifications for FIXED terms under 5 years and VARIABLE mortgages at the discounted contract rate. There was also NO LIMIT for your GROSS DEBT SERVICING (GDS) if your credit was strong enough. Relaxed lending guidelines when debt servicing secured and unsecured lines of credits and heating costs for non-subject and subject properties.

July 2008

We saw the elimination of 100% financing, the decrease of amortizations from 40-35 years and the introduction of minimum required credit scores, which all took place during this time period. It was also the time in which the Total Debt Servicing (TDS) could only be maxed to 45%.

April 2010

This time period saw Variable Rate Mortgages having to be qualified at the 5-year Bank of Canada’s posted rate along with 1-4 year Fixed Term Mortgages qualified at the same. There was also the introduction of a minimum of 20% down vs. 5% on investment properties and an introduction of new guidelines on looking at rental income, property taxes and heat.

March 2011

The 35-year Amortization dropped to 30 years for conventional mortgages, refinancing dropped to 85% from 90% and the elimination of mortgage insurance on secured lines of credit.

July 2012

30-year amortizations dropped again to 25 years for High Ratio Mortgages (less than 20% down). Refinancing also dropped down this time to 80% from 85%. Tougher guidelines within stated income mortgage products making financing for the Business for Self more challenging and the disappearance of true equity lending. Perhaps the three biggest changes of this time were:

Ban mortgage insurance on any million dollar homes

20% min requirement for down payment

Elimination of cash back mortgages

Federal guidelines Min; requirement of 5% down

Introduction to FLEX DOWN mortgage products

February 2014

Increase in default insurance premiums.

February 2016

Minimum down payment rules changed to:

Up to $500,000 – 5%

Up to $1 million – 5% for the first $500,000 and 10% up to $1 million

$1 million and greater requires 20% down (no mortgage insurance available)

Exemption for BC Property Transfer Tax on NEW BUILDS regardless if one was a 1st time home buyer with a purchase price of $750,000 or less.

July 2016

Still fresh in our minds, the introduction of the foreign tax stating that an ADDITIONAL 15% Property Transfer Tax is applied for all non residents or corporations that are not incorporated in Canada purchasing property in British Columbia.

October 17, 2016: Stress testing

INSURED mortgages with less than 20% down Have to qualify at Bank of Canada 5 year posted rate.

November 30, 2016: Monoline Lenders

Portfolio Insured mortgages (monoline lenders) greater than 20% have new conditions with regulations requiring qualification at the Bank of Canada 5 year posted rate, maximum amortization of 25 years, max purchase price of $1 million and must be owner-occupied.

AND HERE WE ARE NOW…

January 2018: OSFI ANNOUNCES STRESS TESTING FOR ALL MORTGAGES + NO MORE BUNDLING AND MORE RESTRICTIONS

If your mortgage is uninsured (greater than 20% down payment) you will now need to qualify at the greater of the five-year benchmark rate published by the Bank of Canada or the contractual mortgage rate +2%

Lenders will be required to enhance their LTV (loan to value) limits so that they will be responsive to risk. This means LTV’s will need to change as the housing market and economic environment change.

Restrictions will be placed on lending arrangements that are designed to circumvent LTV limits. This means bundled mortgages will no longer be permitted.

*A bundled mortgage is when you have a primary mortgage and pair it with a second loan from an alternative lender. It is typically done when the borrower is unable to have the required down payment to meet a specific LTV.

WHERE DO WE GO FROM HERE?

As you can see, the industry has always been one that has changed, shifted and altered based on the economy and what is currently going on in Canada. However, with the new changes that have come into effect this year, we recognize that many are concerned about the financial implications the 2018 changes may have.

The one piece of advice that we promised you at the start of this blog, and one that has helped all our clients get through these changes is this: work with a Dominion Lending Centres mortgage broker!

We cannot emphasize the importance of this enough. We have up to date, industry knowledge, access to all of the top lenders and we are free to use! We guarantee to not only get you the sharpest rate, but also the right product for your mortgage.